.jpeg)

승계 CEO 체제하의 전략적 ESG 행동: CEO의 정치적 및 환경적 경험 관점

Strategic ESG Behavior Under Successor CEOs: CEOs' Political and Green Experience Perspective

1 연세대학교

2 서울시립대학교

1 Yonsei University

2 University of Seoul

DOI: https://doi.org/10.17287/kmr.2026.55.1.387

초록

본 연구는 CEO 승계가 전략적 환경·사회·지배구조(ESG) 행동, 특히 ESG 공시와 실질적인 기업 관행 사이의 괴리에 미치는 영향을 조사한다. 2010년부터 2022년까지 중국 상장 기업의 패널 데이터를 활용하여, 승계 CEO가 이끄는 기업이 전략적 ESG 활동에 참여할 가능성이 유의미하게 더 높음을 입증한다. 나아가, 본 연구는 개별 경영진의 정치적 및 환경 관련 경험이 이러한 관계를 어떻게 조절하는지 조사한다. 분석 결과, 승계와 전략적 ESG 행동 사이의 정(+)의 관계는 정치적 연결고리나 환경적 배경이 부족한 CEO들 사이에서 더 두드러지게 나타났다. 이는 외부 자원에 대한 접근성과 확립된 전문적 명성이 순수하게 상징적인 ESG 참여에 대한 유인을 완화할 수 있음을 시사한다. 또한, 이러한 효과는 외부 모니터링 메커니즘이 덜 견고한 기관 투자자 지분율이 낮은 기업에서 증폭된다. 이러한 결과는 기업 고정 효과 모델, 도구 변수 추정 및 엔트로피 균형법을 포함한 다양한 강건성 테스트를 통해서도 일관되게 나타났다. 본 연구는 CEO 승계를 전략적 ESG 행동의 핵심 결정 요인으로 식별하고 경영진의 배경과 기업 지배구조 환경의 조건부 역할을 강조함으로써 ESG 및 리더십 교체에 관한 문헌에 기여한다.

Abstract

This study examines the impact of CEO succession on strategic Environmental, Social, and Governance (ESG) behavior—specifically the divergence between ESG disclosures and substantive corporate practices. Utilizing a panel dataset of Chinese listed firms from 2010 to 2022, the research demonstrates that firms led by successor CEOs are significantly more inclined to engage in strategic ESG actions. Furthermore, this study investigates how individual executive political and green-related experience, moderate this relationship. The results indicate that the positive association between succession and strategic ESG behavior is more pronounced among CEOs lacking political connections or green backgrounds. This suggests that access to external resources and established professional reputations may mitigate the incentives for purely symbolic ESG engagement. Additionally, the effect is amplified in firms with lower institutional ownership, where external monitoring mechanisms are less robust. These findings are resilient to various robustness checks, including firm fixed-effects models, instrumental variable estimation, and entropy balancing. This research contributes to the literature on ESG and leadership transitions by identifying CEO succession as a critical determinant of strategic ESG behavior and highlighting the contingent roles of executive backgrounds and corporate governance environments.

Ⅰ. Introduction

With the global shift toward sustainability, stakeholders have become increasingly concerned about corporate ESG practices (Kang et al., 2024). They are calling on firms to proactively disclose relevant environmental, social, and governance (ESG) information (Khatib, 2024). In the absence of a standardized ESG disclosure framework and effective regulatory enforcement, firms enjoy substantial discretion in how and what ESG information they report. This regulatory gap has led to opportunistic behavior in ESG practices, with some firms engaging in impression management by overemphasizing ESG disclosures without allocating adequate resources to actual ESG performance. This creates a discrepancy between reported and actual ESG practices—a phenomenon referred to as strategic ESG behavior (Yu et al., 2020).

Strategic ESG behavior undermines a firm’s long-term sustainable development, distorts capital market resource allocation, and poses risks to various stakeholders. For instance, it can damage corporate reputation and erode social support (Gatti et al., 2021; Huh et al., 2025), impair capital allocation efficiency (Liu et al., 2024), and harm overall societal welfare (Delmas and Burbano, 2011). Given the potential societal and financial consequences, understanding the conditions under which firms engage in strategic ESG behavior is both theoretically and practically important.

Scholars have examined the drivers of strategic ESG behavior, identifying both external and internal influences. External factors include institutional changes such as environmental tax reform (Hu et al., 2023) and the expiration of government subsidies (Zhang, 2023b), while internal factors involve governance mechanisms like board composition (Yu et al., 2020), digital transformation (Sun et al., 2025), and the presence of CSR committees (Gull et al., 2023a). Among these factors, recent studies have emphasized the influential role of the CEO in shaping ESG strategy (Sauerwald and Su, 2019; Gull et al., 2023b; Liu et al., 2024), drawing on upper echelons theory, which posits that organizational outcomes reflect the characteristics and values of top executives (Hambrick and Mason, 1984; Chung and Lee, 2024). However, existing research has primarily focused on static CEO characteristics, such as gender, education, or political ties, whereas the dynamic process of leadership change remains underexplored.

Leadership transitions, especially CEO turnover, represent critical events that may reshape firm strategies and decision-making processes (Karaevli, 2007) and potentially trigger shifts in ESG priorities and implementation.

For successor CEOs, the pressure to demonstrate effective leadership within a short period is coupled with the challenge of balancing the diverse expectations of multiple stakeholders (Chen et al., 2019). As Hambrick et al. (2005) noted, in complex decision-making environments and demanding role expectations, CEOs are more likely to exhibit bounded rationality, relying on cognitive shortcuts and making decisions within a limited scope of information search. Consequently, these decision-making patterns are inherently shaped by individual characteristics (Hambrick, 2007).

On one hand, managerial defense theory posits that newly appointed CEOs may reduce symbolic ESG behavior and instead emphasize transparency and substantive ESG engagement to preserve legitimacy. This strategy not only helps them establish credibility and avoid reputational risk but also signals a long-term orientation toward value creation (Erhart, 2022). On the other hand, from agency theory and impression-management perspectives, successor CEOs may face heightened career concerns and time pressure to produce immediate results. In response, they may engage in strategic ESG behavior—such as embellishing sustainability disclosures—as a cost-effective means of projecting a favorable image and gaining stakeholder approval (Yu et al., 2020; Chen et al., 2023). Therefore, the effect of CEO succession on strategic ESG behavior remains theoretically ambiguous and warrants further empirical investigation. These competing theoretical perspectives highlight the ambiguity of the impact of CEO succession on ESG behavior, which calls for systematic empirical research.

To explore this question, we conduct an empirical analysis using a panel dataset of Chinese listed firms from 2010 to 2022. China, as the world’s largest developing economy, has placed increasing emphasis on sustainable development and ESG-related reform. However, the country’s relatively weak regulatory framework for ESG disclosure creates ample room for opportunistic behavior by firms, making it a particularly suitable setting to examine how newly appointed CEOs approach ESG strategy. Our analysis reveals that CEO succession is positively associated with strategic ESG behavior. This finding supports the impression management perspective, suggesting that newly appointed CEOs, facing intense career pressure and limited time to demonstrate performance, may be inclined to overstate their sustainability efforts as a low-cost means of building legitimacy. Our results are robust across multiple empirical strategies, including firm fixed effects and two-stage least squares (2SLS) estimation to address potential endogeneity, as well as entropy balancing methods to account for sample imbalance.

Moreover, we explore the moderating roles of CEO political experience and green-related career background in shaping the relationship between successor CEOs and strategic ESG behavior. The results indicate that the positive association is significantly weaker when the successor CEO has prior political experience, suggesting that access to external policy resources and government support may mitigate career-related pressures, thereby diminishing the incentive to engage in symbolic ESG actions. In addition, we find that the positive relationship is also attenuated among successor CEOs with green-related experience, such as prior roles in environmental organizations or sustainability-focused industries. These CEOs, already perceived as pro-sustainability, may be less motivated to rely on greenwashing to signal ESG commitment.

We also conduct a series of cross-sectional tests to deepen our understanding of the regression outcomes. We first examine whether the positive effect of CEO succession on strategic ESG behavior differs between firms with high and low institutional ownership. Institutional investors are known for their monitoring role and emphasis on ESG transparency. Our cross-sectional analysis reveals that the positive association between successor CEOs and strategic ESG behavior is more pronounced in firms with low institutional ownership, where external oversight is weaker, and CEOs have greater discretion over ESG disclosures.

Our findings make several significant contributions to the existing literature. First, this study adds to the literature on the determinants of strategic ESG behavior. By focusing on the CEO as the key decision-maker for ESG policies, we offer a new perspective on how CEO succession affects firms’ engagement in strategic ESG practices. Our study also expands the use of upper echelon theory by shifting the focus from static executive characteristics to dynamic leadership changes (Karaevli, 2007). Second, while existing research suggests that successor CEOs tend to increase voluntary ESG disclosures (Chen et al., 2023), we argue that such disclosures may not always reflect genuine ESG efforts. By examining ESG misalignment, we contribute to the growing body of research on the unintended consequences of leadership changes, particularly in relation to non-financial strategic actions. Finally, we find that inherent personal experiences of successor CEOs, such as political ties and green-related backgrounds, significantly influence the relationship between CEO succession and strategic ESG behavior. These findings underscore the importance of considering individual career backgrounds when evaluating CEO-driven ESG strategies, demonstrating that the credibility and motivations of ESG initiatives can vary significantly based on executive experience. Our results shed light on how individual-level differences can either amplify or mitigate symbolic ESG engagement in the early stages of a CEO's tenure.

The subsequent sections of this study are structured as follows: Section 2 reviews relevant literature and develops hypotheses. Section 3 describes the sample, data, and research design. Sections 4 and 5 present the empirical findings and additional analyses. Finally, Section 6 concludes the study by summarizing key insights and implications.

II. Literature Review and Hypothesis Development

2.1 Determinants of Strategic ESG Behavior

Strategic ESG behavior refers to a company’s actions related to ESG that do not align with its actual performance, such as false reporting, selective disclosure, or intentionally omitting important ESG information. These practices can have significant consequences, including the erosion of social trust (Gatti et al., 2021), inefficiencies in resource allocation (Liu et al., 2024), and harm to overall societal welfare (Delmas and Burbano, 2011). In response to the increasing prevalence and risks associated with strategic ESG behavior, scholars have explored its antecedents from multiple perspectives.

A substantial body of research has investigated how internal firm characteristics (e.g., firm size, performance, organizational capacity) and external influences (e.g., pressure from governments, NGOs, or market stakeholders such as consumers) shape firms’ propensity to engage in strategic ESG behavior (Delmas and Montes-Sancho, 2010; Delmas and Burbano, 2011; Kim and Lyon, 2015; Blome et al., 2017; Yu et al., 2020; Zhang, 2022). For example, Kim and Lyon (2015) find that large firms under strict regulatory scrutiny are more likely to engage in strategic ESG practices to protect their reputations; however, the presence of environmental NGOs mitigates this tendency. Delmas and Montes-Sancho (2010) show that as consumer environmental awareness grows, firms may strategically deploy ESG narratives to meet perceived green demands and gain competitive advantages. Additionally, Zhang (2022), using a sample of Chinese manufacturing firms, finds that highly polluting firms are more likely to adopt strategic ESG practices to alleviate financing constraints under green financial regulations. Similarly, Blome et al. (2017), based on 118 German multinational corporations aligned with sustainability standards, demonstrate that strategic ESG behavior is influenced by the leadership style of authoritative organizational leaders.

In recent years, a growing body of research has shifted its focus to executive characteristics, revealing that CEO power (Gull et al., 2023b), CEO overconfidence (Sauerwald and Su, 2019), CEO poverty experiences (Liu et al., 2024), and other individual attributes can significantly impact ESG-related decisions. However, most of these studies assume that the CEO’s identity and preferences remain constant over time. In reality, with the professionalization of the Chinese labor market and intensifying market competition, CEO turnover has become a strategic mechanism in corporate governance. However, little is known about whether and how successor CEOs influence strategic ESG behavior, leaving a critical gap in the literature.

2.2 Economic Consequences of CEO Succession

As the central component of a firm’s human capital, the CEO plays a pivotal role in shaping corporate strategy. Different CEOs possess distinct cognitive frameworks and strategic orientations, which can have profound and lasting effects on firm outcomes. Consequently, CEO succession is widely regarded as a critical corporate event (Hambrick and Mason, 1984).

Prior studies have proposed two primary hypotheses regarding the economic consequences of CEO succession. The ability hypothesis (Bonnier and Bruner, 1989; Huson et al., 2004; Pessarossi and Weill, 2013) posits that new CEOs possess superior managerial capabilities compared to their predecessors, especially those associated with poor firm performance. As a result, CEO turnover is interpreted by the market as a positive signal that managerial change will lead to improved firm outcomes. In contrast, the scapegoat hypothesis (Efendi et al., 2013) posits that firm performance is influenced by a combination of managerial effort and random external shocks (Kim, 1996). Therefore, a CEO may be replaced not because of personal shortcomings, but simply to appease stakeholders after poor performance. In this case, CEO succession does not convey new information about the firm’s prospects.

Given the uncertainty surrounding how capital markets interpret CEO turnover, successor CEOs often face career-related concerns and may adopt strategic behaviors to signal their leadership quality. These behaviors may include initiating mergers and acquisitions (Li et al., 2017), manipulating earnings (Ali and Zhang, 2015; Bolor-Erdene and Yoo, 2024), or engaging in aggressive tax avoidance (Li et al., 2022) to boost short-term firm performance and market perception. Ali and Zhang (2015) demonstrate that CEOs are more likely to overstate earnings during the early stages of their tenure, when their capabilities are under scrutiny. Similarly, Li et al. (2022) find that career-concerned CEOs are more inclined to engage in tax avoidance to garner favorable evaluations from their current employers.

As stakeholder expectations continue to evolve, the performance evaluation paradigm for CEOs has expanded beyond traditional financial indicators, such as shareholder returns and firm value, to include non-financial metrics like ESG performance (Hubbard et al., 2017). Recent studies suggest that strong ESG outcomes can enhance a CEO’s reputation in the executive labor market. For example, Cohen et al. (2023) find that the number of firms worldwide incorporating ESG metrics into executive KPIs is rapidly increasing. Dai et al. (2023) show that CEOs of firms with strong CSR performance are more likely to secure future leadership positions. This implies that the managerial labor market rewards ESG-conscious behavior during a CEO’s tenure. In this context, a growing body of literature has examined how career concerns shape executive decisions related to environmental governance and corporate social responsibility (CSR) disclosure. Chen et al. (2023) find that CEOs in the early stage of their tenure are more likely to voluntarily issue standalone CSR reports that disclose how they engage with stakeholders in the decision-making process, reflecting reputational motivations. Given the signaling incentives associated with CEO succession and the increasing salience of ESG performance in executive evaluations, it remains unclear whether successor CEOs are more likely to engage in authentic ESG efforts or strategic, symbolic ESG behavior. This study aims to address this gap.

2.3 Hypothesis Development

According to managerial defense theory, successor CEOs facing complex and uncertain environments may reduce strategic ESG activities as a form of self-protection to preserve their position and legitimacy (Boeker, 1997). First, successor CEOs may perceive enhancing ESG transparency and authenticity as a critical tool to establish their leadership credibility. By improving ESG practices and disclosure quality, they signal competence and ethical standards to the board and shareholders (Erhart, 2022), thereby mitigating internal pressure and consolidating their authority. Second, as stakeholder demands for transparency grow and ESG scrutiny intensifies, engaging in strategic ESG behavior—particularly symbolic or misleading actions—may pose serious reputational and legal risks for these CEOs. To avoid punitive consequences, they may become more cautious and limit symbolic ESG engagement. Third, in light of ESG’s growing role in investment decisions and firm valuation, successor CEOs may recognize that substantive ESG improvements contribute to sustainable competitive advantage. By prioritizing authentic ESG integration over symbolic gestures, such CEOs can demonstrate that the company is evolving toward more responsible and sustainable leadership. This not only reinforces their perceived integrity (Erhart, 2022) but also signals their ability to balance value creation with ESG responsibilities, enhancing their market credibility and long-term career prospects. In light of the theoretical perspectives outlined above, this study advances the following hypothesis:

Hypothesis 1a: Successor CEOs are less likely to engage in strategic ESG behavior.

Conversely, from an agency perspective, successor CEOs may be incentivized to increase strategic ESG behavior to manage impressions and enhance their legitimacy. CEO turnover often reflects the board’s dissatisfaction with prior performance (Puffer and Weintrop, 1991), placing high pressure on these CEOs to produce visible outcomes within a limited time and resources (Chen, 2015). From an attention-based view, these executives tend to focus more on short-term financial performance—where failure can lead to immediate dismissal—rather than on long-term ESG investments (Harrison and Fiet, 1999). Investing heavily in ESG without immediate returns may even be interpreted by the board as a misalignment with shareholder interests (Hubbard et al., 2017). Moreover, poor ESG perception has become a growing trigger for CEO dismissal in sustainability-sensitive markets (Chiu and Sharfman, 2018), compelling successor CEOs to build a sustainability image quickly (Chen et al., 2023). In this context, greenwashing—or the strategic manipulation of ESG disclosure—can become an appealing tactic, as it creates a favorable image at relatively low cost (Yu et al., 2020; Kim et al., 2021). Ultimately, given that substantive ESG improvements require long-term commitment and resource investment, successor CEOs seeking job security may allocate limited resources to financial performance while selectively employing symbolic ESG actions to balance their short-term career advancement goals with the firm’s long-term sustainability trajectory. Therefore, this study also proposes the hypothesis that:

Hypothesis 1b: Successor CEOs are more likely to engage in strategic ESG behavior.

Ⅲ. Methodology and Data

3.1 Data and Sample Selection

This study’s sample comprises all Chinese A-share companies listed on the Shanghai and Shenzhen Stock Exchanges from 2010 to 2022. Following the literature, firms in the financial sector1), those classified as ST or *ST2), and those with missing ESG or other financial data are excluded from the analysis. The final sample includes 1,231 unique firms and 8,783 firm-year observations. All continuous variables are winsorized at the 1% and 99% levels to mitigate potential outliers. 〈Table 1〉

Table 1 Sample Composition and Selection Procedure

| Panel A: Breakdown by Industry | ||

|---|---|---|

| Industry classification | Firm-years | Percent (%) |

| Agriculture, forestry, fishery, and animal husbandry | 126 | 1.43 |

| Coal, oil, natural gas, metals, and nonmetallic mining | 345 | 3.93 |

| Manufacturing | 5,315 | 60.51 |

| Electricity, heating, gas, water production, and supply | 360 | 4.10 |

| Construction | 297 | 3.38 |

| Wholesale and retail trade | 477 | 5.43 |

| Transportation, warehousing, and postal services | 403 | 4.59 |

| Accommodation and catering | 13 | 0.15 |

| Information transport, Internet, software, and information technology services | 528 | 6.01 |

| Real estate, leasing, and business services | 529 | 6.02 |

| Education, health, sports, and entertainment | 258 | 2.93 |

| Scientific research, environmental management, public utilities, and other industries | 132 | 1.50 |

| Total | 8,783 | 100 |

| Panel B: Breakdown by Year | ||

| Year | Firm-years | Percent (%) |

| 2010 | 458 | 5.21 |

| 2011 | 550 | 6.26 |

| 2012 | 606 | 6.90 |

| 2013 | 666 | 7.58 |

| 2014 | 632 | 7.20 |

| 2015 | 772 | 8.79 |

| 2016 | 687 | 7.82 |

| 2017 | 710 | 8.08 |

| 2018 | 772 | 8.79 |

| 2019 | 833 | 9.48 |

| 2020 | 815 | 9.28 |

| 2021 | 856 | 9.75 |

| 2022 | 426 | 4.85 |

| Total | 8,783 | 100 |

| Panel C: Sample Selection Procedure | ||

| Description | Count | |

| Chinese A-share listed companies on the Shanghai and Shenzhen Stock Exchanges from 2010 to 2022 | 41,622 | |

| Less: Financial firms | -1,185 | |

| Less: Firms with missing ESG data | -29,394 | |

| Less: Firms with ST, *ST, and missing other financial data | -2,260 | |

| Final Sample | 8,783 |

Note:

Given that only approximately 19% of executives’ resumes are disclosed in the “Board and Executive Characteristics” section of the China Stock Market and Accounting Research (CSMAR) database (Huang and Guo, 2024), we undertook extensive efforts to manually collect and organize CEO resumes from companies’ financial reports and official websites. Specifically, we thoroughly examined the collected resumes to identify individuals with political and environmental backgrounds. The ESG rating data are sourced from the Wind database, firm-level variables are compiled from the CSMAR database, and regional-level data are derived from the statistical yearbooks of various provinces in China.

3.2 Variable Definition

3.2.1 Dependent Variable: strategic ESG behavior

The primary dependent variable in this study is corporate strategic ESG behavior (StrategicESG), which reflects the divergence between a firm’s ESG disclosures and its actual ESG practices. Following the methodology proposed by Yu et al. (2020) and Zhang (2023a), we measure this construct by calculating the difference between disclosure-based and practice-based ESG scores. Specifically, we operationalize strategic ESG behavior as the value obtained by subtracting the Practice ESG score (measured by Hua Zheng ESG) from the Disclosure ESG score (measured by Bloomberg ESG). Higher values indicate a greater degree of symbolic or strategic ESG behavior, suggesting firms may be overstating their ESG performance through selective or exaggerated disclosure. The detailed computation is presented in Equation (1).

We use the Bloomberg ESG disclosure score to capture the extent of ESG information voluntarily disclosed by firms (Tamimi and Sebastianelli, 2017; Yu et al., 2018; Liao et al., 2023; Qu, 2024). Bloomberg evaluates disclosure using a bottom-up, model-driven approach, based on publicly available sources, including ESG reports, CSR reports, annual filings, proxy statements, corporate governance reports, and official company websites. The scoring system comprises three primary categories, 20 subcategories, and more than 120 indicators, encompassing both quantitative items (e.g., NOx emissions) and qualitative aspects (e.g., whether the firm has a climate change policy). In total, Bloomberg’s ESG framework comprises more than 900 disclosure items, which are aggregated into a composite score ranging from 0 to 100. A higher score indicates a greater volume and comprehensiveness of ESG disclosure, but it does not directly reflect the quality or substance of ESG performance.

To capture firms’ actual ESG practices, we adopt the Hua Zheng ESG score (Chatterji et al., 2016; Berg et al., 2022; Ma and Yu, 2023; Zhang, 2023a). Hua Zheng provides an ESG rating system specifically designed for the Chinese capital market and the unique characteristics of Chinese listed firms. Its indicator framework integrates both explicit responsibilities (e.g., charitable donations, employee welfare, poverty alleviation, and rural revitalization) and implicit responsibilities, such as macro-level contributions to economic and employment stability during crises (e.g., financial downturns or public health emergencies). Unlike many international ESG rating agencies, Hua Zheng incorporates uniquely Chinese dimensions that are often overlooked in global frameworks. The system employs an industry-adjusted scoring method that classifies firms into nine grades (AAA to C), with scores ranging from 0 to 100. This performance-oriented score serves as a proxy for firms’ substantive ESG engagement.

3.2.2 Independent Variable: Successor CEO

In this study, the CEO is defined as the individual holding the position of general manager, president, or chief executive officer in a listed company. The variable $SuccessorCEO$ is coded as 1 if a CEO succession occurs in a given year and 0 otherwise. In addition, if a firm experiences, this study considers the successor CEO for that year.

3.3 Empirical Model

Hypothesis 1 is tested with the following Equation (2):

$StrategicESG_{i,t/t+1} = \beta_0 + \beta_1 SuccessorCEO_{i,t} + \sum \beta_n Controls_{i,t} + Fixed Effect + \varepsilon_{i,t}$ (2)

where the subscripts $i$ and $t$ refer to the firm and year, respectively. The dependent variable is the firm’s strategic ESG behavior ($StrategicESG_{i,t/t+1}$), measured either in the same year as the CEO succession ($t$) or in the following year ($t+1$), which helps us capture both immediate and slightly delayed responses to leadership change.

The key independent variable of interest is $SuccessorCEO_{i,t}$.

Controls are the set of control variables commonly used in prior strategic ESG studies.

Building on prior research (Jin et al., 2024), we examine several firm financial characteristics that may influence a firm’s strategic ESG behavior. These factors encompass firm size (Size), leverage (Lev), return on assets (ROA), firm age (Age), state ownership (Soe), board size (Boardsize), board independence (Indep), ownership concentration (Top10), duality (Dual), market-to-book ratio (MB), and economic development level (GDP). This study further controls for CEOs’ individual characteristics, including CEO age (CEOAge), CEO education (CEODegree), and CEO gender (CEOGender). We incorporate industry (Industry) and year (Year) fixed effects to control for industry-and time-specific factors.

Additionally, we employ robust standard errors and firm-level clustering adjustments in all OLS regression models to enhance the robustness of our findings (Petersen, 2008). The variables utilized to test the hypothesis are detailed in <Appendix A>, with a particular focus on the significant coefficient $\beta_1$ in Eq. (2).

Ⅳ. Empirical Results

4.1 Descriptive Statistics

Table 2 Descriptive Statistics

| Variables | N | Mean | SD | Min | Median | Max |

|---|---|---|---|---|---|---|

| StrategicESG | 8,783 | -0.319 | 1.159 | -2.636 | -0.431 | 3.086 |

| SuccessorCEO | 8,783 | 0.169 | 0.375 | 0 | 0 | 1 |

| Size | 8,783 | 23.153 | 1.309 | 19.887 | 23.047 | 26.314 |

| Lev | 8,783 | 0.471 | 0.199 | 0.056 | 0.481 | 0.913 |

| ROA | 8,783 | 0.048 | 0.061 | -0.280 | 0.042 | 0.195 |

| Age | 8,783 | 12.161 | 7.130 | 1 | 12 | 28 |

| Soe | 8,783 | 0.471 | 0.499 | 0 | 0 | 1 |

| Boardsize | 8,783 | 8.986 | 1.797 | 5 | 9 | 14 |

| Indep | 8,783 | 37.451 | 5.450 | 33.330 | 35.710 | 57.140 |

| Top10 | 8,783 | 60.559 | 15.931 | 22.200 | 60.870 | 90.240 |

| Dual | 8,783 | 0.229 | 0.420 | 0 | 0 | 1 |

| MB | 8,783 | 3.478 | 3.235 | 0.514 | 2.443 | 20.013 |

| GDP | 8,783 | 10.485 | 0.764 | 6.231 | 10.539 | 11.768 |

| CEOAge | 8,783 | 50.693 | 6.160 | 28 | 51 | 75 |

| CEODegree | 8,783 | 3.795 | 1.179 | 1 | 4 | 7 |

| CEOGender | 8,783 | 0.932 | 0.251 | 0 | 1 | 1 |

Note:

strategic ESG behavior ($StrategicESG$) is -0.319, indicating that, on average, firms in our sample tend to perform better in ESG practices than in ESG disclosure. This pattern aligns with previous findings (e.g., Jin et al., 2024) and may indicate relatively conservative ESG disclosure practices, particularly among firms that engage in meaningful ESG activities but underreport them due to limited transparency incentives or weak disclosure standards. The minimum value of $StrategicESG$ is -2.636, and the maximum is 3.086, indicating substantial variation in strategic ESG engagement across firms. Regarding CEO succession, the mean value of $SuccessorCEO$ is 0.169, indicating that approximately 16.9% of the sample firms experienced a change in CEO during the observation period. Regarding the personal characteristics of successor CEOs, 22.9% also serve as board chairpersons, and the majority are male, with an average education level above the undergraduate level. The summary statistics for the remaining control variables are generally consistent with findings in prior empirical research.

The un-tabulated Pearson correlation test indicates a significantly positive correlation between $SuccessorCEO$ and $StrategicESG$, providing preliminary evidence that firms led by successor CEOs are more likely to engage in strategic ESG behavior.

4.2 Main Regression Results

Table 3 Impact of Successor CEO on Strategic ESG Behavior

| Variables | (1) Dependent variable = $StrategicESG_{i,t}$ | (1) t-stat. | (2) Dependent variable = $StrategicESG_{i,t+1}$ | (2) t-stat. |

|---|---|---|---|---|

| Coefficient | Coefficient | |||

| Intercept | -4.387*** | -6.193 | -4.828*** | -6.943 |

| SuccessorCEO | 0.094*** | 3.057 | 0.052** | 2.180 |

| Size | 0.188*** | 6.208 | 0.229*** | 9.103 |

| Lev | 0.355** | 2.182 | 0.084 | 0.517 |

| ROA | -1.390*** | -4.050 | -2.861*** | -14.789 |

| Age | 0.015*** | 3.577 | 0.017*** | 5.708 |

| Soe | -0.160*** | -2.911 | -0.180*** | -5.651 |

| Boardsize | 0.008 | 0.553 | 0.005 | 0.394 |

| Indep | -0.011*** | -2.626 | -0.013** | -2.813 |

| Top10 | 0.007*** | 4.257 | 0.007*** | 3.451 |

| Dual | 0.068 | 1.286 | 0.101** | 2.550 |

| MB | 0.031*** | 4.297 | 0.036*** | 8.305 |

| GDP | -0.026 | -0.760 | -0.045** | -2.139 |

| CEOAge | -0.008** | -1.998 | -0.006** | -2.760 |

| CEODegree | 0.025 | 1.527 | 0.022*** | 3.480 |

| CEOGender | 0.070 | 0.892 | 0.049 | 0.456 |

| Industry FE | YES | YES | ||

| Year FE | YES | YES | ||

| Observations | 8,783 | 7,619 | ||

| Adjusted $R^2$ | 0.102 | 0.088 |

Note:

In both specifications, the coefficient on $SuccessorCEO$ is positive and statistically significant, indicating that firms led by successor CEOs are more likely to engage in strategic ESG behavior. Specifically, the coefficient in Column (1) is 0.094 (t-stat. = 3.057), and remains significant in Column (2) at 0.052 (t-stat. = 2.180), suggesting that the effect is not limited to immediate disclosures but extends into the following fiscal year.

This finding provides empirical support for the argument that successor CEOs may strategically manipulate ESG disclosures to enhance their reputations or signal leadership effectiveness, particularly in the early stages of their tenure, when career-related concerns are heightened. Overall, these findings underscore the importance of leadership transitions in shaping firms’ non-financial disclosure strategies and highlight the symbolic use of ESG as a strategic tool by newly appointed executives.

Ⅴ. Additional Analyses and Robustness Tests

5.1 Moderator Analysis: How Does the Successor CEO Impact Strategic ESG Behavior?

The main results indicate that firms led by successor CEOs are more likely to engage in strategic ESG behavior. We attribute this finding to the career concerns faced by newly appointed CEOs. CEO turnover is often prompted by the board’s dissatisfaction with prior performance (Puffer and Weintrop, 1991), placing successor CEOs under significant pressure to deliver visible and immediate results within a limited timeframe and with constrained resources, in order to avoid dismissal (Chen, 2015). Moreover, in sustainability-sensitive markets, poor ESG perception has become an increasingly important factor contributing to CEO turnover (Chiu and Sharfman, 2018), further motivating newly appointed CEOs to quickly construct a favorable sustainability image (Chen et al., 2023). Therefore, in this section, we further examine whether two career-related considerations moderate the positive association between CEO succession and strategic ESG behavior. Specifically, we conduct subgroup regressions and compare the estimated coefficients of $SuccessorCEO$ across groups to examine whether politically connected successor CEOs and those with environmentally relevant personal backgrounds differ in their likelihood of engaging in strategic ESG behavior. A visual summary of the group-wise effects is provided in <Appendix B>.

5.1.1 CEO Political Experience

A CEO’s political experience provides access to valuable policy resources, government subsidies, and preferential treatment, especially in institutional environments where the state plays an active role in resource allocation and regulation (Faccio, 2006; Fan et al., 2007; Li et al., 2008; Goldman et al., 2009; Wu et al., 2012). Such connections help firms alleviate short-term financial constraints (Fan et al., 2011), thus easing the immediate performance pressure that often burdens newly appointed CEOs.

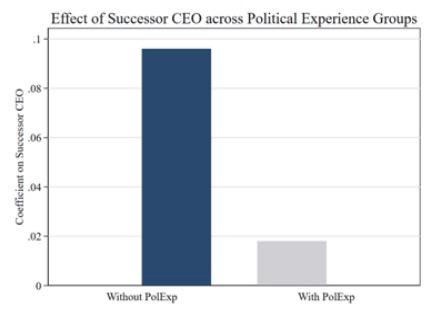

From a career-concerns perspective, politically connected successor CEOs are less likely to fear dismissal, as their external legitimacy and resource-mobilization capacity provide an implicit guarantee of leadership capital. As a result, these CEOs have less incentive to rely on symbolic ESG behavior to build a favorable public image or to prematurely signal competence. Instead, their political ties serve as a substitute for ESG-based reputation building. In contrast, non-politically connected successor CEOs, who lack these institutional advantages, may feel greater pressure to utilize symbolic ESG practices to construct a sustainability narrative and establish their standing. Therefore, we predict that the positive relationship between successor CEOs and strategic ESG behavior is weaker when the CEO has political experience.

To test this prediction, we divide the sample into two subgroups based on CEO political background: firms with politically experienced CEOs and those without. Following Fan et al. (2007) and Zhang et al. (2025b), a politically experienced CEO is defined as one whose CEO or Vice-CEO has previously held or currently holds a position in government-related roles, including as a central or local government official, a member of the Chinese People’s Political Consultative Conference (CPPCC), or a deputy to the National People’s Congress (NPC), or military officers.3)

Table 4 Moderating Effect of the CEO’s Political Experience

| Variables | Dependent variable = $StrategicESG_{i,t}$ | |||

|---|---|---|---|---|

| (1) With political experience | (2) Without political experience | |||

| Coefficient | t-stat. | Coefficient | t-stat. | |

| Intercept | -5.582*** | -4.745 | -4.241*** | -4.611 |

| $SuccessorCEO$ | 0.018 | 0.313 | 0.096** | 2.253 |

| $Size$ | 0.234*** | 4.811 | 0.154*** | 4.047 |

| $Lev$ | 0.045 | 0.163 | 0.442** | 2.278 |

| $ROA$ | -2.051*** | -3.181 | -1.076** | -2.375 |

| $Age$ | 0.013* | 1.738 | 0.017*** | 3.148 |

| $Soe$ | 0.001 | 0.010 | -0.245*** | -3.475 |

| $Boardsize$ | -0.021 | -0.912 | 0.032* | 1.651 |

| $Indep$ | -0.018*** | -2.641 | -0.005 | -0.848 |

| $Top10$ | 0.008*** | 3.046 | 0.008*** | 3.519 |

| $Dual$ | 0.065 | 0.653 | 0.081 | 1.163 |

| $MB$ | 0.027* | 1.854 | 0.032*** | 3.334 |

| $GDP$ | 0.019 | 0.306 | -0.020 | -0.472 |

| $CEOAge$ | -0.000 | -0.063 | -0.010* | -1.825 |

| $CEODegree$ | 0.041* | 1.754 | 0.029 | 1.241 |

| $CEOGender$ | 0.194 | 1.563 | 0.025 | 0.210 |

| Industry FE | YES | YES | ||

| Year FE | YES | YES | ||

| Observations | 2,890 | 4,611 | ||

| Adjusted $R^2$ | 0.125 | 0.111 | ||

| Diff. | -0.078*** |

Note:

3) After excluding observations with missing data on political experience, the sample used for this test comprises 7,501 firm-year observations, of which 2,890 are classified as having CEOs with political experience and 4,611 as not.

5.1.2 CEO Green Experience

Successor CEOs with a green-related professional background (e.g., prior experience in sustainability, CSR, or environmental policy roles) often enter the position with a pre-established environmental reputation (Hu and Shi, 2025). Their existing identity as environmentally responsible leaders reduces the need to signal a green image through symbolic ESG actions. Moreover, these CEOs may be more committed to authentic ESG goals and less likely to engage in manipulative or misleading disclosures, as such practices could undermine their prior reputations and personal credibility. In contrast, CEOs without such backgrounds lack a pre-existing green image. They may feel a stronger need to construct one quickly, thereby increasing their propensity to engage in symbolic ESG behavior as a signaling strategy. Therefore, the positive relationship between successor CEOs and strategic ESG behavior is likely to be more pronounced when the CEO lacks a background in green-related careers.

Referring to Javed et al. (2023) and Quan et al. (2023), the CEO’s green experience is characterized by their educational background or work experience. Specifically, we measured green experience by assessing whether the CEO has received education in green-related fields or has worked in green-related fields. The former is assessed based on whether the CEO’s major is pulp and paper, environmental engineering, or environmental science (Li et al., 2024). The latter is evaluated based on whether the CEO has worked for the Ministry of Environmental Protection or the Environmental Protection Committee, or has held a position overseeing environmental pollution control within an enterprise (Li et al., 2024). Similarly, we divide the sample into two subgroups based on whether the CEO has a green-related career background and re-estimate Eq. (2) separately for each subgroup.4

4 The test sample includes 8,652 firm-year observations after excluding missing data on green experience, with 787 involving CEOs with green experience and 7,865 without.

Table 5 Moderating Effect of the CEO’s Green Experience

| Variables | Dependent variable = $StrategicESG_{i,t}$ | |||

|---|---|---|---|---|

| (1) With green experience | (2) Without green experience | |||

| Coefficient | t-stat. | Coefficient | t-stat. | |

| Intercept | -6.484*** | (-3.308) | -3.927*** | (-5.430) |

| $SuccessorCEO$ | 0.013 | (0.120) | 0.090*** | (2.747) |

| $Size$ | 0.184** | (2.340) | 0.178*** | (5.641) |

| $Lev$ | 1.184** | (2.175) | 0.335** | (1.973) |

| $ROA$ | 1.414 | (1.079) | -1.504*** | (-4.266) |

| $Age$ | 0.007 | (0.493) | 0.015*** | (3.452) |

| $Soe$ | -0.343** | (-1.991) | -0.147** | (-2.565) |

| $Boardsize$ | 0.066 | (1.197) | 0.008 | (0.562) |

| $Indep$ | 0.028** | (1.991) | -0.014*** | (-3.287) |

| $Top10$ | 0.012*** | (2.610) | 0.007*** | (4.271) |

| $Dual$ | 0.011 | (0.067) | 0.072 | (1.310) |

| $MB$ | -0.007 | (-0.315) | 0.033*** | (4.301) |

| $GDP$ | -0.085 | (-0.788) | -0.024 | (-0.694) |

| $CEOAge$ | -0.010 | (-0.783) | -0.007* | (-1.776) |

| $CEODegree$ | 0.107 | (1.590) | 0.028 | (1.616) |

| $CEOGender$ | 0.268 | (0.816) | -0.097 | (-1.178) |

| Industry FE | YES | YES | ||

| Year FE | YES | YES | ||

| Observations | 787 | 7,865 | ||

| Adjusted R^2 | 0.182 | 0.103 | ||

| Diff. | -0.077*** |

Note:

5.2 Cross-sectional Analysis: Institutional Ownership

Institutional investors are often regarded as sophisticated and influential stakeholders who play a crucial monitoring role in corporate governance (Bushee, 2001; Gillan and Starks, 2003). Companies with significant institutional ownership are subject to greater external scrutiny, particularly regarding ESG performance and disclosure (Dyck et al., 2019). Consequently, successor CEOs in these companies face tighter oversight and fewer opportunities to undertake symbolic or strategic ESG actions without being noticed.

In contrast, when institutional ownership is relatively low, firms face weaker monitoring, giving CEOs more discretion in shaping disclosure practices. Successor CEOs in such settings may have greater freedom to strategically manage ESG narratives to signal competence or to build a sustainability image early in their tenure, especially when formal ESG performance metrics take longer to emerge. Therefore, we expect the positive link between CEO succession and strategic ESG behavior to be stronger when institutional ownership is low.

We split the sample into two subgroups based on the level of institutional ownership. Firms with institutional shareholding above the median were classified as high institutional ownership (High IO), while those below the median were classified as low institutional ownership (Low IO). We re-estimated Eq. (2) for each subgroup, and the results are shown in Table 6

Table 6 Cross-sectional Analysis: Institutional Ownership

| Variables | Dependent variable = $StrategicESG_{i,t}$ | |||

|---|---|---|---|---|

| (1) High IO | (2) Low IO | |||

| Coefficient | t-stat. | Coefficient | t-stat. | |

| Intercept | -2.283** | -2.239 | -5.534*** | -5.967 |

| $SuccessorCEO$ | 0.045 | 1.025 | 0.111*** | 2.602 |

| Controls | YES | YES | ||

| Industry FE | YES | YES | ||

| Year FE | YES | YES | ||

| Observations | 4,444 | 4,339 | ||

| Adjusted $R^2$ | 0.079 | 0.138 | ||

| Diff. | -0.066*** |

Note:

As shown in Columns (1) and (2) of Table 6

As shown in Columns (1) and (2) of Table 6, the coefficient on $SuccessorCEO$ is positive and statistically significant in the low institutional ownership group (coefficient = 0.111, t-stat. = 2.602), while the coefficient is not statistically significant in the high institutional ownership group. These results support our argument that in firms with lower institutional ownership, monitoring mechanisms are less stringent, allowing successor CEOs greater discretion to engage in symbolic ESG practices, thereby enhancing their reputation and demonstrating leadership legitimacy. In contrast, in firms with high institutional ownership, stricter monitoring and accountability lessen the likelihood of such symbolic actions, thereby weakening the influence of CEO succession on strategic ESG engagement.

5.3 Robustness Tests

To validate the robustness of our findings, we conduct several tests: controlling for predecessor CEO characteristics and firm fixed effects, using two-stage least squares method, and applying entropy-balancing estimation. The results are presented in Table 7

Table 7 Robustness Tests

| Panel A: Controlling for Predecessor CEO Characteristics | ||||

| Variables | Dependent variable = $StrategicESG_{i,t}$ | |||

| Coefficient | t-stat. | |||

| Intercept | -4.135*** | -5.564 | ||

| $SuccessorCEO$ | 0.121*** | 3.343 | ||

| $Lag\_CEOAge$ | -0.003 | -0.688 | ||

| $Lag\_CEODegree$ | 0.031* | 1.668 | ||

| $Lag\_CEOGender$ | 0.034 | 0.349 | ||

| Controls | YES | |||

| Industry FE | YES | |||

| Year FE | YES | |||

| Observations | 7,488 | |||

| Adjusted $R^2$ | 0.103 | |||

| Panel B: Controlling for Firm Fixed Effects | ||||

| Variables | Dependent variable = $StrategicESG_{i,t}$ | |||

| Coefficient | t-stat. | |||

| Intercept | 3.951* | 1.651 | ||

| $SuccessorCEO$ | 0.055* | 1.895 | ||

| Controls | YES | |||

| Firm FE | YES | |||

| Industry FE | YES | |||

| Year FE | YES | |||

| Observations | 8,783 | |||

| Adjusted $R^2$ | 0.458 | |||

| Panel C: Using Two-Stage Least Squares Method | ||||

| Variables | Dependent variable = $SuccessorCEO$ | Dependent variable = $StrategicESG_{i,t}$ | ||

| 1st Stage | 2nd Stage | |||

| Coefficient | t-stat. | Coefficient | t-stat. | |

| Intercept | 0.748*** | 6.465 | -6.467*** | -6.807 |

| $CEORetire Age$ | 0.038*** | 3.530 | ||

| $SuccessorCEO\_hat$ | 2.641*** | 3.073 | ||

| Controls | YES | YES | ||

| Industry FE | YES | YES | ||

| Year FE | YES | YES | ||

| Observations | 8,783 | 8,783 | ||

| Adjusted $R^2$ | 0.052 | 0.082 | ||

| Cragg-Donald Wald F-statistic | 31.02*** | |||

| Durbin-Wu-Hausman test of endogeneity | 1.147 | |||

| Panel D: Applying Entropy Balancing Method | ||||

| Variables | Dependent variable = $StrategicESG_{i,t}$ | |||

| Coefficient | t-stat. | |||

| Intercept | -4.944*** | -6.046 | ||

| $SuccessorCEO$ | 0.084*** | 2.730 | ||

| Controls | YES | |||

| Industry FE | YES | |||

| Year FE | YES | |||

| Observations | 8,783 | |||

| Adjusted $R^2$ | 0.112 |

Note:

5.3.1 Controlling for Predecessor CEO Characteristics

First, a potential concern is that the characteristics of the previous CEO may influence the successor’s strategic ESG behavior. This influence can occur through mechanisms such as path dependence in strategic direction or organizational imprinting, shaped by the former CEO’s values and practices, which can either constrain or guide the incoming CEO's decisions. Therefore, to capture individual-level influences that might persist beyond leadership changes, we include lagged CEO-level controls as proxies for the outgoing CEO’s characteristics. Specifically, we incorporate the predecessor CEO’s age, education level, and gender ($Lag\_CEOAge$, $Lag\_CEODegree$, $Lag\_CEOGender$), based on the CEO in office during year t-1, and analyze the subsample with available lagged CEO data. As shown in Panel A of Table 7, the coefficient on $SuccessorCEO$ remains positive and statistically significant at the 1% level (coefficient = 0.121, t-stat. = 3.343), indicating that our main results are robust to inclusion of predecessor CEO traits.

5.3.2 Controlling for Firm Fixed Effects

Second, to account for unobserved, time-invariant firm-level characteristics that may confound the relationship between CEO succession and strategic ESG behavior, we include firm fixed effects, in addition to industry and year fixed effects. As shown in Panel B of Table 7, the coefficient on $SuccessorCEO$ remains positive and statistically significant at the 10% level (coefficient = 0.055, t-stat. = 1.895), suggesting that the main finding is robust even after controlling for firm-level heterogeneity.

5.3.3 Using the Two-Stage Least Squares Method

Third, in our primary empirical analysis, we treat $SuccessorCEO$ as an exogenous variable, assuming unobserved firm-level factors do not influence it. However, this assumption may be challenged, as CEO succession decisions could be driven by unobservable characteristics such as internal governance dynamics, firm culture, or anticipated ESG strategies. To address potential endogeneity concerns—particularly those arising from omitted variable bias—we employ a two-stage least squares (2SLS) estimation as an additional robustness check.

Table 7, Panel C, presents the 2SLS estimation results. In the first stage, we instrument $SuccessorCEO$ with $CEORetire Age$, a variable indicating whether the CEO reached the mandatory retirement age in China. This variable is strongly correlated with CEO turnover and provides plausibly exogenous variation in CEO succession. The first-stage regression shows that $CEORetire Age$ is positively and significantly associated with $SuccessorCEO$. The first-stage Cragg-Donald Wald F-statistic is 31.02, exceeding the conventional threshold of 10, confirming the strength of the instrument. In the second stage, the fitted values of $SuccessorCEO$ remain significantly and positively associated with $StrategicESG$ (coefficient = 2.641, t-stat. = 3.073), lending further support to the causal interpretation of our findings.

5.3.4 Applying the Entropy Balancing Method

Finally, we employ the entropy balancing method to address potential covariate imbalance between firms with and without CEO succession. This semi-parametric reweighting technique ensures that the treatment and control groups are balanced with respect to observable covariates prior to regression analysis (Hainmueller, 2012). As shown in Panel D of Table 7, the results continue to reveal a significantly positive association between $SuccessorCEO$ and $StrategicESG$ (coefficient = 0.084, t-stat. = 2.730), thereby supporting the robustness of our findings under an alternative sample balancing framework.

Ⅵ. Conclusion

6.1 Summary of Findings

This study investigates whether successor CEOs influence corporate strategic ESG behavior. Using panel data from Chinese listed firms, our findings suggest that companies led by successor CEOs are more likely to exhibit strategic ESG behavior. We attribute this pattern to the heightened career concerns and performance pressure faced by newly appointed CEOs. With limited time and resources, successor CEOs tend to prioritize short-term financial results while maintaining a sustainability image through symbolic ESG practices. These results align with prior research indicating that newly appointed CEOs may employ impression-management strategies, such as greenwashing, to protect their positions (Ali and Zhang, 2015).

Furthermore, we find that this positive relationship is attenuated when CEOs possess political or green-related experience, as such backgrounds may alleviate career pressure and reduce the need for symbolic ESG signaling. Politically connected CEOs are more likely to access external government resources and subsidies, thereby easing financial constraints. Likewise, CEOs with environmentally relevant backgrounds already have a pro-sustainability image, which reduces the incentive to artificially boost ESG disclosure.

6.2 Discussions

Our findings underscore the significance of leadership changes as a governance event that can profoundly affect a firm’s ESG strategy, particularly through symbolic actions. By linking CEO succession to strategic ESG behavior, this study contributes to the growing body of research on executive influence in ESG decision-making. Additionally, our results extend the upper echelons theory by demonstrating that the effect of CEO traits on firm behavior evolves rather than remaining constant. In particular, newly appointed CEOs may intentionally engage in symbolic ESG actions to shape perceptions and earn stakeholder approval. This supports the idea that CEOs act as “agents of legitimacy,” especially during the vulnerable early period of their leadership when external criticism and internal uncertainty are at their peak.

An alternative explanation is that the gap between ESG disclosure and practice reflects a temporary misalignment rather than a deliberate strategy. For instance, newly appointed CEOs may initially be unfamiliar with internal operations, ESG systems, or data reporting processes, which can lead to unintentional discrepancies early in their tenure. However, several patterns in our findings indicate this explanation is inadequate. First, ESG disclosure in our context is voluntary mainly and requires intentional managerial effort, thereby signaling strategic intent. Second, we observe that the effect is notably stronger among successor CEOs with political connections or experience in green-related fields, traits typically associated with career incentives and reputational concerns. This pattern supports the view that successor CEOs deliberately engage in symbolic ESG behavior to enhance legitimacy during a leadership transition.

These findings have several practical implications. Firms undergoing CEO succession should be aware of the potential ESG risks associated with leadership changes. Although some transition-related friction may occur, the evidence suggests a deliberate and strategic process. Boards should stay alert to the reputational motives and career concerns of successor CEOs and develop ESG-related incentives that promote genuine, long-term sustainability efforts. Aligning ESG objectives with executive compensation can help newly appointed CEOs adopt a long-term outlook and recognize the strategic importance of ESG.

Additionally, we discover that robust external governance and stakeholder oversight can help limit shallow ESG actions. We advise stakeholders to include ESG-related clauses in CEO contracts to prevent greenwashing and improve accountability for meaningful ESG results. Finally, creating balanced performance assessment systems is crucial to prevent CEOs from focusing solely on short-term financial goals at the expense of long-term environmental and social objectives.

6.3 Limitations and Future Research

Despite the robustness of our empirical results, this study is subject to several limitations that offer opportunities for future research.

First, while the construction of strategic ESG provides a meaningful way to identify differences between ESG disclosure and actual practice, the two ESG ratings used in this calculation (i.e., Bloomberg ESG for disclosure and Hua Zheng ESG for practice) are not “pure” indicators of either disclosure or substantive performance. Although Bloomberg’s approach prioritizes narrative ESG disclosure from voluntary corporate reports and public filings, and Hua Zheng focuses on measurable ESG actions and policy outcomes, both systems inevitably overlap. This is because ESG ratings are inherently composite indicators lacking a universally accepted definition, and their methodologies are often proprietary and multidimensional (Berg et al., 2022). For instance, Bloomberg’s disclosure score may partially reflect actual practices when performance is prominently reported, while Hua Zheng’s practice score could be affected by the transparency and accessibility of firm disclosures. Therefore, our measure of strategic ESG captures a directional gap between disclosure and performance but does not fully separate the two domains.

We recommend that future research develop or incorporate more refined ESG metrics that can better distinguish narrative disclosure from actual ESG actions. This might include combining text-based disclosure analysis with objective performance measures or exploring alternative ESG evaluation sources using transparent, domain-specific methods. Such improvements would lead to a more accurate assessment of the distinction between symbolic and substantive ESG efforts, providing a stronger basis for examining firms' strategic motives in sustainability reporting.

Second, while our study focuses on Chinese listed firms, the institutional and regulatory environment in China may limit the generalizability of our findings. The strategic use of ESG may vary substantially across countries due to differences in disclosure regimes, investor pressure, and stakeholder expectations. Future research could apply our framework to other emerging or developed markets to assess the consistency of these patterns in varying institutional settings.

Moreover, although we consider a range of CEO background traits, including political experience and green-related expertise, unobservable qualities such as leadership style, ethical orientation, or personal values may also affect ESG decisions, as Mason and Hambrick (1984) suggest. Future research may examine additional personal traits or use survey-based data to investigate deeper behavioral drivers of strategic ESG choices.

Finally, the symbolic use of ESG disclosure may be front-loaded at the beginning of a CEO's tenure and then gradually decrease as their tenure lengthens, and the organization's credibility stabilizes. Clarifying whether strategic ESG behavior is truly a temporary, career-driven tactic or a lasting feature of executive leadership remains an important area for future research. Future studies could empirically examine this pattern by including interaction terms between CEO tenure and strategic ESG behavior, or by using longitudinal data to observe how disclosure-practice divergence changes over time.

〈Appendix A〉 Variables Definition

〈Appendix B〉 Visual Graphs for Moderator Analyses - Section 5.1

To visually present the effect of CEO succession on strategic ESG behavior across subgroups defined by CEO background characteristics, we present bar plots showing the estimated coefficients for $SuccessorCEO$ across two subsamples. Panel A compares firms led by successor CEOs with and without political experience, while Panel B compares those with and without green experience. These graphs supplement the subgroup regression results reported in Section [

Panel A: CEO Political Experience Graph

Appendix A Variables Definition

| Variables | Description |

|---|---|

| StrategicESG | Corporate strategy ESG behavior: the divergence between a firm’s ESG disclosures (Bloomberg ESG) and actual ESG practices (Hua Zheng ESG) |

| SuccessorCEO | A dummy variable that is one if a CEO succession occurs in year t, and zero otherwise |

| Size | The natural logarithm of total assets |

| Lev | The ratio of total liabilities to total assets |

| ROA | The net income divided by total assets |

| Age | The number of years since a firm’s initial public offering (IPO) |

| Soe | A dummy variable that is one if the firm is government-controlled, and zero otherwise |

| Boardsize | The number of board directors |

| Indep | The proportion of independent outside directors to the total number of directors |

| Top10 | The percentage of shareholdings held by the top 10 shareholders |

| Dual | A dummy variable equal to one if the chief executive officer (CEO) and chairperson are the same person, and zero otherwise |

| MB | The market value of equity plus the book value of debt divided by total assets |

| GDP | Economic development level: the natural logarithm of regional per capita GDP |

| CEOAge | The age of the CEO at the end of the fiscal year |

| CEODegree | CEO educational level is categorized as PhD = 5, Master’s degree = 4, Bachelor’s degree = 3, Associate degree = 2, and below associate level = 1 |

| CEOGender | A dummy variable equal to one if the CEO is male and zero if the CEO is female |

| Industry FE | Industry fixed effect |

Table 9

| Year FE | Year fixed effect |

|---|---|